All Categories

Featured

Table of Contents

Tax lien investing can give your profile exposure to realty all without needing to in fact possess residential or commercial property. Specialists, nevertheless, claim the process is made complex and advise that newbie financiers can easily obtain melted. Below's whatever you require to know regarding spending in a tax obligation lien certification, consisting of just how it works and the risks involved.

The notification normally comes before harsher activities, such as a tax levy, where the Internal Earnings Solution (INTERNAL REVENUE SERVICE) or local or local governments can actually seize a person's residential or commercial property to recover the financial debt. A tax lien certificate is developed when a homeowner has actually fallen short to pay their tax obligations and the regional government issues a tax lien.

Tax obligation lien certifications are usually auctioned off to investors looking to revenue. To recover the overdue tax obligation dollars, communities can after that offer the tax obligation lien certification to personal financiers, who deal with the tax obligation costs in exchange for the right to gather that cash, plus passion, from the homeowner when they eventually repay their balance.

Tax Lien Investing Expert

permit the transfer or assignment of overdue property tax liens to the personal field, according to the National Tax Lien Association, a nonprofit that represents federal governments, institutional tax obligation lien investors and servicers. Here's what the process looks like. Tax obligation lien financiers have to bid for the certificate in an auction, and how that process works depends on the specific municipality.

Contact tax officials in your location to make inquiries exactly how those delinquent tax obligations are collected. The town establishes a maximum price, and the bidder supplying the cheapest rate of interest rate underneath that optimum wins the auction.

Other winning proposals most likely to those that pay the highest possible money quantity, or costs, over the lien quantity. What takes place following for capitalists isn't something that happens on a stock market. The winning bidder has to pay the whole tax expense, consisting of the delinquent financial obligation, rate of interest and penalties. The capitalist has to wait until the home proprietors pay back their entire balance unless they don't.

While some capitalists can be compensated, others could be caught in the crossfire of complicated policies and technicalities, which in the most awful of conditions can bring about large losses. From a mere profit perspective, a lot of financiers make their money based on the tax lien's rate of interest. Passion prices differ and depend on the jurisdiction or the state.

Revenues, nevertheless, do not always amount to yields that high during the bidding procedure. Ultimately, many tax liens bought at auction are sold at rates between 3 percent and 7 percent across the country, according to Brad Westover, executive director of the National Tax Obligation Lien Association. Before retiring, Richard Rampell, formerly the chief executive of Rampell & Rampell, an accounting company in Hand Coastline, Florida, experienced this firsthand.

Investing In Tax Liens And Deeds

At first, the partners succeeded. Then huge institutional capitalists, consisting of banks, hedge funds and pension plan funds, went after those greater returns in auctions around the country. The bigger capitalists assisted bid down rate of interest, so Rampell's team wasn't making substantial cash anymore on liens. "At the end, we weren't doing better than a CD," he claims - investing in tax liens in texas.

That seldom takes place: The taxes are usually paid before the redemption date. Liens likewise are initial eligible repayment, even prior to home mortgages. Also so, tax obligation liens have an expiry day, and a lienholder's right to confiscate on the residential property or to accumulate their investment expires at the exact same time as the lien.

Individual financiers that are taking into consideration investments in tax liens should, over all, do their homework. Experts suggest preventing properties with environmental damage, such as one where a gas station disposed unsafe material.

What Is Tax Lien Certificate Investing

"You need to actually understand what you're getting," states Richard Zimmerman, a companion at Berdon LLP, an accounting company in New york city City. "Know what the property is, the community and worths, so you do not buy a lien that you will not be able to gather." Potential capitalists must additionally inspect out the residential or commercial property and all liens versus it, in addition to current tax sales and price of similar buildings.

Keep in mind that the info you discover can typically be outdated. "People obtain a checklist of homes and do their due diligence weeks before a sale," Musa claims. "Fifty percent the buildings on the checklist might be gone because the taxes earn money. You're losing your time. The closer to the date you do your due persistance, the far better.

Investing In Tax Lien

Westover says 80 percent of tax obligation lien certificates are sold to participants of the NTLA, and the agency can frequently match up NTLA members with the appropriate institutional capitalists. That might make managing the process simpler, especially for a newbie. While tax lien investments can provide a generous return, understand the small print, information and policies.

"However it's made complex. You need to recognize the information." Bankrate's contributed to an upgrade of this story.

Residential property tax liens are a financial investment specific niche that is overlooked by most financiers. Buying tax liens can be a lucrative though reasonably danger for those that are educated regarding real estate. When individuals or businesses stop working to pay their residential property taxes, the districts or other federal government bodies that are owed those tax obligations place liens versus the residential properties.

Tax Lien Tax Deed Investing

These insurance claims on collateral are additionally traded among capitalists who intend to produce above-average returns. With this process, the community obtains its tax obligations and the financier obtains the right to collect the quantity due plus interest from the borrower. The process rarely finishes with the investor taking ownership of the residential property.

If you need to confiscate, there may be other liens against the home that keep you from taking ownership. You can likewise invest indirectly through home lien funds.

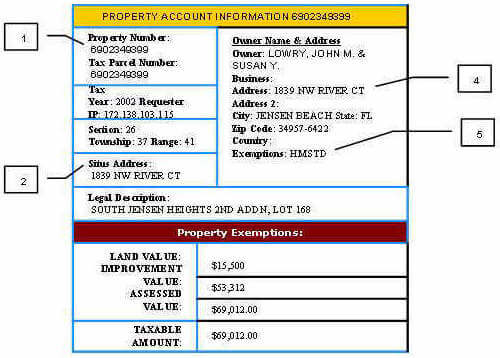

It properly locks up the residential property and stops its sale until the owner pays the tax obligations owed or the building is taken by the financial institution. For instance, when a landowner or property owner fails to pay the taxes on their property, the city or area in which the building lies has the authority to place a lien on the home.

Residential property with a lien connected to it can not be sold or re-financed till the tax obligations are paid and the lien is removed. When a lien is provided, a tax lien certification is created by the municipality that reflects the amount owed on the residential property plus any kind of passion or charges due.

It's estimated that an additional $328 billion of residential property taxes was assessed across the United state in 2021. It's hard to evaluate across the country residential property tax obligation lien numbers.

{kind=link}

Latest Posts

List Of Tax Lien Properties

Tax Lien Foreclosures

Back Owed Property Taxes